@SwissRe.

@SwissRe.

More persistent inflation is forging an interest rate regime shift.

Finally "risk-free" sovereign bond rates are not return-free anymore. The real interest rates adjustment continues as inflation pressure remains very high: bad for financial markets today, but good for the pricing of risk longer-term.

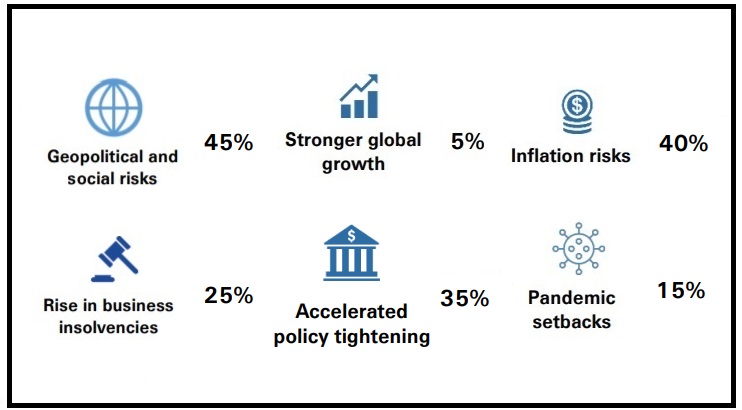

Inflation continues to surprise the upside. We see significant pipeline pressures stemming from multi-decade-high producer price inflation, which rose again in April. Commodity and food price pressure and supply-chain disruptions are also persisting as geopolitical tensions go on. Accelerated, more aggressive monetary policy tightening by the US Federal Reserve (Fed) and ECB is expected in response.

We expect central banks to frontload rate hikes as slowing growth narrows the window of opportunity to bring inflation under control. We now expect the Fed to hike rates by 50bps at each of the next two meetings for a total of 250bps tightening this year, and another 50bps next year, as well as its stated quantitative tightening (QT).

We expect the ECB to tighten the deposit rate by a total of 75bps and the refinancing rate by 50bps this year and tighten both rates by another 25bps next year, with the first rate hike starting with just the deposit rate this July. APP purchases will also end shortly before.

Our growth forecasts continue to be below consensus as the war in Ukraine and COVID-19 restrictions in China choke off global external demand and push up cost-of-living.

We revise down our 2022 and 2023 real GDP growth forecast for China to 4.6% and 5%. Our baseline outlook is "stagflation-like", with high inflation and low but still positive annual GDP growth, but recession outcomes in several key economies, notably the euro area but also the US, over the next 12 months are now more likely.

If needs be, central banks may well prioritise addressing inflation over growth, especially as labour markets remain tight.

The combination of high inflation and policy tightening is driving long-term sovereign bond yields higher in major markets – the end of the era of negative nominal interest rates.

In a sea change for our rates view, we revise up advanced market yield forecasts significantly, with US 10-year Treasury yields expected at 2.8% at end-2022 and 2.9% at end-2023.

The prospect of both QT by major central banks, and global low-yield anchors such as the ECB and Bank of Japan exiting ultra-low-rate policy, create further upside risk for yields.

Uncertainty is high around the future of the war in Ukraine and escalation could trigger further trade sanctions.

Higher energy, fuel and food prices are exacerbating the cost-of-living crisis, which in turn could aggravate social tensions and spark unrest.

Risks to growth in Europe from embargoes on Russian energy exports is particularly high.

Key to watch: Russia-West tensions, economic sanctions, US-China disputes, US mid-term elections.

Inflation pressure in major markets is high and becoming more persistent. Supply-side drivers of inflation, such as energy, food prices and disruption to other commodity supply chains are not expected to abate soon, and labour markets are tightening.

The longer inflation persists, the higher the likelihood that expectations will become self-fulfilling.

Key to watch: euro area HICP (18 May), US PCE (27 May), supply bottlenecks, energy crisis, more persistent inflation categories (eg, rents), wages.

Higher, more persistent inflation is prompting more aggressive monetary policy tightening.

The costs associated with inflation and tight labour markets are so high that central banks may keep pace with tightening even if the economic slowdown is more severe than anticipated this year and recessions materialise.

Key to watch: central bank speeches; inflation expectations; further fiscal announcements; capital flows from/into EMs.

The likelihood of stagflation and recession facing the global economy has increased significantly.

The risk of business insolvencies has risen amid the expected lower growth outlook and higher interest rates, and as pandemic support measures are withdrawn.

These risks are skewed to the upside should financial conditions tighten more sharply that currently anticipated.

Key to watch: Business bankruptcies, credit spreads, restructuring/default rate news, debt servicing costs (interest rates).

The latest COVID-19 wave in China is a reminder that the pandemic and economic disruption is not over, with the risk particularly high for countries pursuing zero tolerance policies.

Such "zero-COVID" strategies come with significant downside risks to growth.

Although the Omicron variant has proven to be mostly milder than prior variants, the emergence of newer and more problematic (eg. vaccine resistant) variants is a possibility.

Key to watch: emergence of more mutations and variants, hospitalisation and death rates, vaccination and booster roll-out rates, anti viral pill treatments, stringency of restrictions and quarantine rules, individual behaviours.

The exit from ultra-accommodative policy could lead to a stronger role for the private sector and investment shifts away from "intangible" assets towards the real economy.

Larger-than-expected fiscal spending as a result of the conflict in Ukraine (eg, in defence and renewable energy infrastructure) could boost growth; resolution of the conflict would also present economic upside.

A stronger-than-expected post-covid rebound in services demand over the summer could also be a near-term boost to European growth. A quicker improvement in productivity due to faster digital adoption or technological breakthroughs would also benefit longer term economic growth.

Key to watch: fiscal spending plans, PMIs, consumption, real interest rates, productivity.