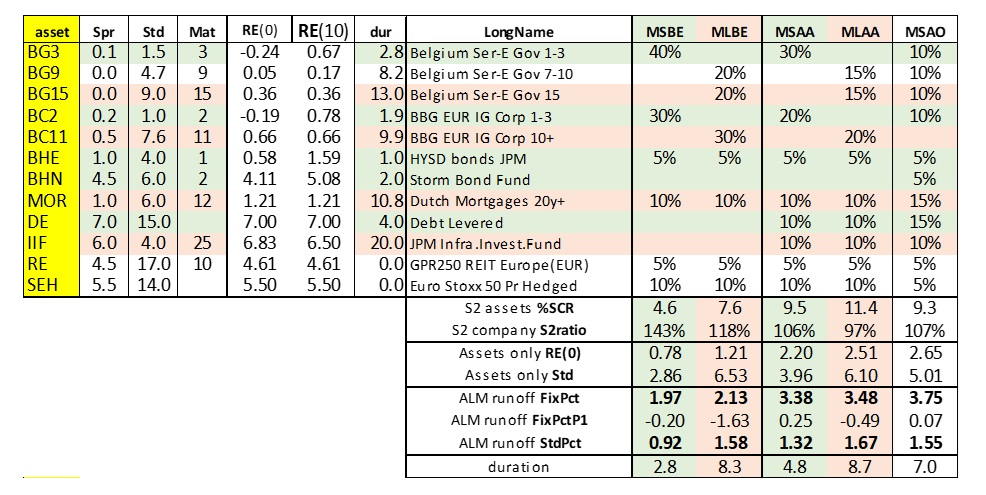

This year's recession could be one of the deepest, but also one of the shortest, on record.

Yet, we shouldn't underestimate the longer-term economic and political implications. Watch out for paradigm shifts.

We expect a global recession with economic activity contracting by 1.2% per cent. The recovery will be protracted, despite massive fiscal stimulus,

The very atypical recession is likely to be more short-lived than others. Global long-term yields will remain low.

Prolonged financial condition tightening poses further downside and increases the risk of a global credit crisis. The risk of a stagflation scenario (>12M) has risen.

We expect a global recession in 2020. The partial economic shutdown is likely to remain in place through most of Q2, assuming new infections in Europe and the US peak in April/May, followed by a gradual return to growth in 3Q (see chart below).

We project an atypical recession which will be twice as deep and more than twice as fast as the Global Financial Crisis (GFC), but relatively short lived.

The subsequent recovery will be protracted. With monetary policy buffers nearly exhausted, fiscal policy is doing the heavy lifting.

On top of liquidity support, we expect significant fiscal stimulus of about 3.1 per cent of global GDP (compared to 1.6 per cent in the GFC) to facilitate recovery in the second half of 2020.

However, this is unlikely to be enough to bring activity back to the previous growth path. We expect the global output loss to amount to about USD 11trn by 2021.

The Covid-19 shock will lead to lower inflation. We expect lower demand to mute price pressures in the near term, but we remain wary of the medium-term inflation risks from a sustained supply shock, which could result in a stagflationary environment.

We expect an increase in "financial repression" with central banks capping yield increases if necessary, to accommodate debt increases. Implicit "yield-curve control" is already happening in the US, in our view.

We project US 10-year yields to close at 1 per cent at year-end, and US Treasury yields may even decline temporarily below 0 per cent.

Yields in Germany will likely remain negative for the foreseeable future unless there is more sharing of debt burdens across the Euro area in the future.

Uncertainties around point forecasts are significant. Scenario thinking is more important than ever, and we see two other, more pessimistic scenarios (see Alternative scenarios and chart b).

A prolonged recession is more likely than a swift recovery, and the risk of "stagflation" has increased given unprecedented fiscal stimulus and potential debt monetisation.

We expect a number of paradigm shifts such as an accelerated adoption of digitalisation, a larger role for governments, and a move towards monetisation of government debt.

Every major crisis marks an inflection point, and the global economic shock from the Covid-19 outbreak is no exception.

We believe the pandemic is likely to trigger several paradigm shifts and bring forward some of the megatrends we previously identified.

The global economy and society may look very different post Covid-19 disruption from what was before.

The extraordinary 2008 playbook of central banks is unfolding again, including quasi direct lending to businesses and implicit yield curve control.

We expect more innovation on the part of central banks if the situation continues to deteriorate.

Ultimately, the only constraint to more central bank innovation is politics, which can be overcome should society explicitly or implicitly demand more action.

Policy measures previously considered unorthodox may well become the norm.

Stimulus such as monetisation of government debt through "helicopter money", will likely also become more normal.

Moves to this end are already underway with several governments vowing to do "whatever it takes", and central banks buying government debt in large and even unlimited quantities.

Besides the US-China trade war, the disruptions across the global supply chain due to the containment measures against Covid-19 will likely translate into companies diversifying their production chains to make them more robust.

This will bring redundancies and become more expensive. The focus will no longer be on finding the cheapest supplier but on ensuring all the different supplies needed are obtained in an efficient and timely manner.

We expect the digitalisation trend to intensify as a result of the Covid-19 containment measures.

For example, many desk-job employees are accessing their company's network remotely and e-commerce companies and platforms become increasingly important.

We expect the Covid-19 experience will only perpetuate trends like these to the extent that they become the "new normal".

Governments have emerged as spenders of last resort. By providing emergency loans and guarantees for business, and by paying salaries and transfers to many individuals, they have taken a much more active role in the economy.

They are unlikely to retreat hastily when the crisis is over. There have already been public injections of capital into and nationalisations of private firms, and we expect more as loans turn into equity stakes and guarantees into bailouts.

After more than two decades of low inflation, the pandemic shock could trigger a turnaround.

Today, the collapse in demand dominates the potential inflationary impact from the supply shock, but this could change over the next few years.

The current shock could result in sharp declines in production, persistent supply chain disruptions and widespread bottlenecks.

Coupled with massive fiscal stimulus, this could result in higher inflation once containment restrictions are lifted.

A trend towards de-globalisation – a major driver of declining inflation in the past – and monetary financing of government debt could amplify inflation risks.

US: The US economy has entered the steepest sharpest recession on record going back to 1950.

We forecast the maximum disruption to activity in 2Q20, followed by a gradual roll-back and return to growth in 3Q20. Record fiscal measures will not be able to offset the sudden stop, but are expected to support an eventual recovery

Euro area: We have lowered our growth projections further with real GDP likely to fall by about 10 per cent during 1H 2020.

Inflation will be lower, too, on the back of suppressed demand. The ECB has announced an additional EUR 750bn of asset purchases and has dropped the issuer limit, which should prevent any immediate sovereign spread widening.

United Kingdom: We expect a recession in the UK in 2020, followed by a sizeable rebound in activity in the following year.

The demand shock will translate into lower prices despite ample fiscal stimulus. The BoE is forecast to keep policy rates on hold, and 10-year yields will drift lower towards year end.

Japan: We now expect an even deeper recession in 2020 than previously, due to Covid-19, as well as the postponement of the Tokyo Olympics to 2021.

The government is preparing additional stimulus measures, while the Bank of Japan (BoJ) has already expanded its QE purchases, doubling its annual ETF target.

China: We have lowered GDP growth to 3.0 per cent in 2020.

The official manufacturing PMI rebounded to 52 in March, reflecting a mild recovery of economic activity.

The PBoC cut RRR by 100bps for targeted sectors and lowered the OMO rate by 20bps to support growth.

Nevertheless, the balance of risks remains skewed to the downside given the severely depressed global demand.